It’s no secret that large chunks of our day-to-day lives have gone digital in the last 10-15 years. Oh sure, we all still work at jobs, live in houses, and drive cars to and fro, but the way that we spend our money, buy our products, invest our wealth, and decide “What’s next?” has changed dramatically. With a single click of a button or swipe of your finger, you can deposit a check into your bank account, order groceries to arrive at your home, get dinner from your favorite restaurant without ever talking to a waiter, and knock out your Christmas shopping without uttering a word. Need a ride to the airport? There’s an app for that. Ditto buying tickets to your favorite new movie, applying for a credit card, securing financing for home repairs, and getting your driver’s license renewed.

Lost in the shuffle of all these minor modern conveniences is the fact that one of the country’s most frustratingly complicated and time-consuming endeavors remains a massive series of paperwork, lengthy in-person appointments, and opportunities for missing and misplaced pages.

Are mortgage companies simply too far behind the curve to join the digital revolution? They are dependent on older technologies that fail miserably when it comes to embracing efficiency and cutting-edge tech. Very few companies have the ability to digitize mortgages, much less the desire to. What’s holding them back and how soon can we expect them to join the digital revolution?

Digital Adoption Overview

Has it only been a decade or so since most businesses were trying not to bump into one another as they scratched their heads about making their websites responsive for this new craze called smartphones and trying to build an application that would offer some sort of convenience beyond the world of desktops? Fast-forward a dozen years and technology has reinvented the landscape of consumers’ lifestyle. If we want a book, we download it to our Kindle. If we need a ride, a few swipes brings a taxi to our driveway, and if you live close enough to an Amazon warehouse facility, the time from order to delivery is starting to drop into the single-digits of hours, rather than days. There have been paradigm shifts in industries that previously experienced decades-long fundamentals because of digital technology. Children used to rush to the toy store for the latest doll, robot, or model, but now they are constantly hitting up Mom and Dad to purchase them the latest app. Gaming itself has changed thanks to digital technology. Once, legions of fans crowded around arcades at the mall to watch the greatest players lay waste to barrel-throwing gorillas and colorful ghosts. Now those legends are making serious bank, raking in advertising dollars as they attract millions of viewers to their YouTube channels.

Technology even changed our lives for the better during the most unprecedented health pandemic the world has seen in a century. Can you imagine what the COVID-19 lockdowns would have been like without Zoom and Netflix and Disney+?

Digital Adoption in Financial Services

Not surprisingly, financial services have long been at the forefront of digital adoption. The ability to move money easily from person to person, and from person to vendor, dates back almost as long as the Internet itself has been a popular thing, with PayPal racing ahead as the early adopter, and Venmo, Zelle, Plaid and others rapidly closing the gap in the last decade. After early growing pains with cybersecurity, these financial instruments have become the most reliable way to move money, turning branches of banks into veritable ghost towns if you’re not trying to secure a loan, and moving us closer and closer to a world without any sort of physical currency at all. Direct deposit, bill pay, and using smartphones to deposit checks with a scanned image have gone from science fiction to mundane everyday activities. By 2019, PayPal was up to 34 million transactions per day.

Digital Adoption in the Loan Industry

Auto Loans

One of the hottest trends in the auto industry in 2021 was the shift to digital auto financing. Digitization in this realm includes digital loan documents, digitization of asset-backed securities (ABS), eSignatures, and more. The COVID-19 pandemic also broke through the stagnant state of mind when car companies had to adapt to make it a customer-centric process. Salesmen began driving to customers’ houses for test drives and sending all that paperwork via secured sites and encrypted emails.

Student Loans

Student loans have followed suit, in large part because the age group who is applying for the overwhelming majority of them is intimately familiar with the technology that powers it. Cutting down on long approval processes with the use of AI allows students to instantly draw on funds as they begin their scholarly endeavors instead of waiting in endless lines at the campus student services offices to have a check cut for them.

SBA Loans

COVID-19 has sped up the shift to digital adoption across industries, and small business banking is no exception. In 2020, Amex acquired Kabbage, a startup that built a whole business around loaning money to SMBs utilizing machine learning algorithms.

Mortgage Industry

In the mortgage industry, KEB Hana Bank, the third largest bank in South Korea, for example, pioneered digitization of mortgage processing with its ‘One Click’ Mortgage, from e-application to e-closing. Sales for Hana Bank’s One Click Mortgage exceeded $2.4 billion ten months after its introduction.

What’s Next?

How can mortgage companies start catching up with KEB Hana’s lead and join the digital revolution being seen across every other major facet of society? If mortgage companies don’t take the lead, larger, national retail lenders will appropriate the process for themselves and put the little guys out of luck. Even more perplexing is that it’s not happening despite research that says switching to digitization can significantly reduce costs.

The biggest obstacle is that companies don’t have the infrastructure or the training to make the switch to digitization. Sure, they can always buy another storage facility for the paper files, but they are limited in their knowledge of cloud technology and not convinced about data security just yet.

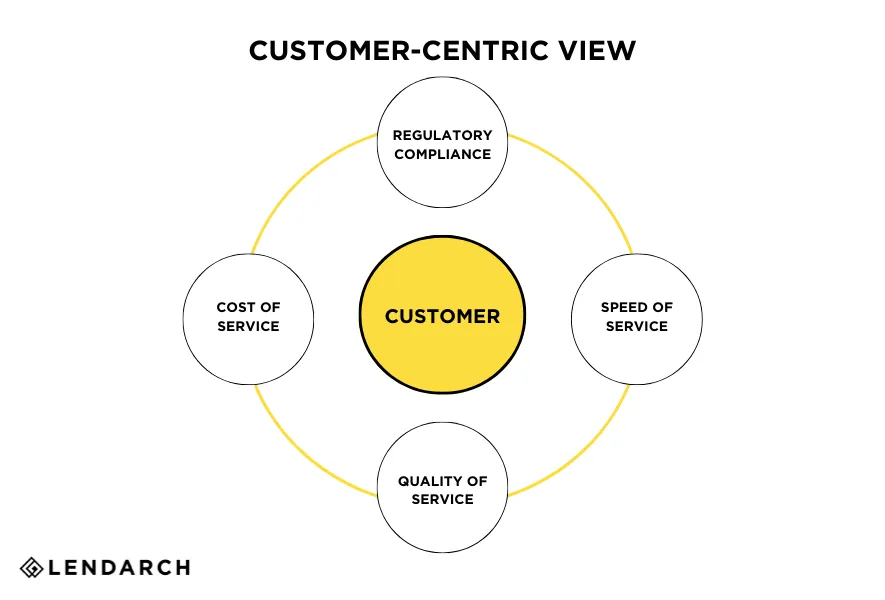

Essentially, effective digital transformation in mortgages comes down to a customer-centric view.

If this view is adopted as your poster for any digital initiative, cross-checking against all the four parameters with your customer as the pivot, your company is on a path to success.

As a leading innovator in this field, LendArch is on a mission to reduce the cost to fulfill through finding efficiencies and end-to-end optimization of the mortgage experience, utilizing artificial intelligence (AI), micro services, and blockchain technology.

If you are looking to take your company to the next level with digitization of the mortgage processes, contact experts at LendArch and we will help you navigate through these objectives by leveraging the best of technologies, digital assets and transformed operations.